What Is a TRF in Banking? Your Quick Guide to Seamless Cross-Border Payments

What Is a TRF in Banking? Your Quick Guide to Seamless Cross-Border Payments

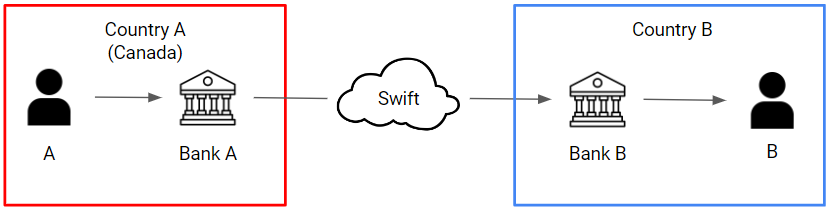

In an era where global transactions define economic connectivity, understanding the TRF — or Triggered Fund — emerges as essential for banks, businesses, and individuals navigating international finance. A TRF is a specialized financial instrument designed to streamline cross-border payments by linking fund releases directly to the fulfillment of predefined conditions, ensuring secure, timely, and traceable transfers. Unlike traditional wire transfers or payment ecosystems tied to settlement schedules, TRFs activate funds only upon verified triggers, significantly reducing counterparty risk and enhancing cash flow predictability.

At its core, a TRF acts as a conditional payment mechanism. Banks or financial institutions initiate the transaction not by immediate settlement, but after confirming that specific criteria—such as delivery confirmation, customs clearance, or contractual milestones—have been met. This conditional disbursement mechanism minimizes defaults and strengthens trust across borders, where delays and opaque processes have historically plagued international trade.

## Core Components and Operational Mechanics A TRF operates through a structured, condition-driven workflow.Each transfer begins with an agreement outlining clear triggers—events validated by mutual recognition between sender and recipient. Common triggers include: - Proof of goods delivery via shipping documents - Verification of service completion by a third-party auditor - Compliance with regulatory checks or trade sanctions - Confirmation of digital contract milestones in fintech contracts Once the trigger is authenticated—often through secure digital verification—funds are released incrementally per condition met. This phased release ensures capital remains locked until obligations are fulfilled, mitigating credit exposure.

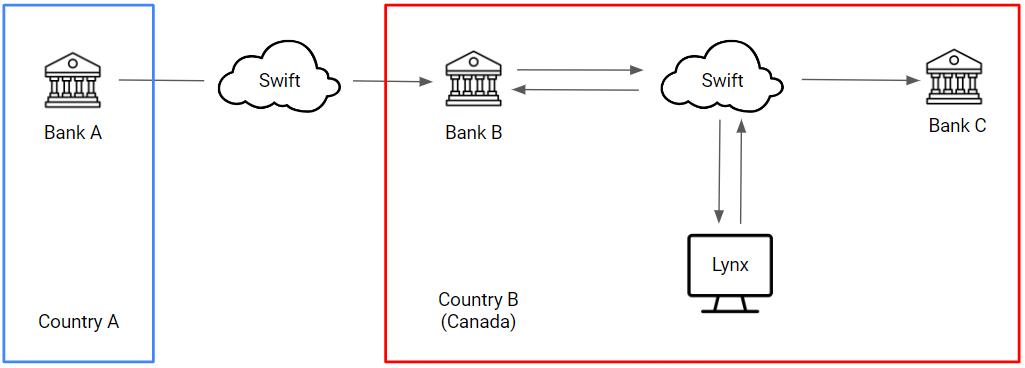

The process relies on interoperable banking systems, real-time data feeds, and compliance protocols that align with both domestic regulations and international standards.

Unlike standard wire transfers, where funds are immediately transferred with settlement occurring later (often days later), TRFs embed settlement timing within the transaction’s logic. This means the fund may not become available until post-verification checkpoints, a dynamic that improves liquidity control for cash-strapped enterprises.

### Key Benefits Driving TRF Adoption The growing popularity of TRFs stems from several transformative advantages: - **Risk Mitigation**: By tying fund release to verified outcomes, TRFs drastically reduce the risk of non-payment and fraud, making them ideal for high-value trade and supply chain finance.- **Enhanced Transparency**: Every release event is logged and auditable, providing stakeholders with real-time visibility into transaction progression. - **Improved Cash Flow Management**: Staggered fund availability aligns disbursements with delivery or service milestones, allowing businesses to better match expenses with incoming receipts. - **Regulatory Compliance**: TRFs support adherence to global anti-money laundering (AML) and know-your-customer (KYC) requirements by embedding compliance checks directly into the transfer logic.

“TRFs represent a paradigm shift in how banks conceptualize cross-border payments,” notes Dr. Elena Kapoor, senior financial systems analyst at the Global Banking Institute. “They merge automation with control—releasing funds only when proof is irrefutable.

This not only cuts operational risk but fundamentally reshapes trust in international finance.” ### Use Cases: When TRFs Shine TRFs are particularly valuable in sectors where accountability and proof are paramount: - **Trade Finance**: Exporters and importers use TRFs to secure payments only after goods clear customs or verification audits. - **Supply Chain Payments**: Automakers and retailers deploy TRFs to release payments upon delivery confirmation from suppliers, reducing working capital strain. - **Insurance and Settlements**: Insurers trigger payouts only after claim validation, ensuring equitable and fraud-resistant settlements.

- **Fintech Integrations**: Digital platforms embed TRF logic to power secure, auto-triggered disbursements tied to service usage or milestone achievement.

For banks, adopting TRF technology requires investment in interoperable infrastructure and data-sharing protocols, but the long-term gains in reducing credit absorption and boosting client trust are compelling. Financial institutions leading TRF adoption report 15–25% lower default rates on cross-border transactions, according to recent industry surveys.

### Challenges and Evolution Despite their advantages, TRFs face hurdles.Legacy banking systems often lack the agility for real-time conditional processing, requiring modernization investments. Cross-jurisdictional differences in regulatory frameworks can complicate trigger validation across borders, especially where data privacy laws diverge. Yet, technological progress is rapidly overcoming these barriers.

The rise of blockchain-based settlement layers, AI-driven document verification, and API-first banking platforms is accelerating TRF deployment. Standardization efforts led by organizations like SWIFT and the International Chamber of Commerce are harmonizing trigger definitions, fostering a more unified global TRF ecosystem. ### The Road Ahead: TRFs as Pillars of Modern Finance TRFs are emerging as more than a technical innovation—they signal a new era of precision in financial transactions.

By embedding accountability directly into the payment workflow, they transform cross-border transfers from uncertain events into predictable, secure exchanges. As global trade increasingly depends on seamless, data-driven interactions, TRFs stand at the intersection of innovation and reliability, empowering institutions to operate with greater agility and trust. The financial landscape is evolving, and the TRF — triggered conditions, guaranteed integrity — is proving essential.

For banks, corporates, and financial systems alike, understanding and implementing TRFs isn’t just an option; it’s a necessity in an interconnected, risk-aware world.

In a time when speed and security define business success, TRFs deliver exactly that—by making every cross-border transaction not just a transfer of funds, but a confirmed achievement. With ongoing advancements and broad industry adoption, Trusted Real-Time Funds (TRFs) are reshaping how value moves across borders, layer by layer, condition by condition.

Related Post

Kelly Ripa’s Divorce Sparks National Conversation on Resilience, Privacy, and the Public’s Right to Know

Master the Grind: How Slice Master’s Idle Clicker Turns Casual Players into Persistent Grinders

Jackson Hole Wy Hotels & Motels: Where Mountain Laziness Meets Urban Comfort

Reviving Classic Gaming: The USB Loader Gx Wii Transforms How We Power Nintendo's Iconic Console