New Construction Home Loan Rates: Your Guide to Securing the Best Rates in 2025

New Construction Home Loan Rates: Your Guide to Securing the Best Rates in 2025

In a dynamic housing market shaped by Federal Reserve policies, inflation trends, and shifting investor sentiment, navigating new construction home loan rates has never been more critical for first-time homebuyers, developers, and investors. As financing costs directly influence affordability and long-term investment viability, understanding the current rate environment—factors affecting pricing, emerging trends, and strategic procurement—is essential. This comprehensive guide delivers actionable insights to help buyers, builders, and planners make informed decisions amid fluctuating market conditions.

Since early 2023, U.S. construction loan rates have reflected broader economic pressures, with prime rates climbing from a historic low of under 2.5% in 2021 to a prevailing range now between 5.5% and 7.5%, depending on loan terms, regional demand, and lender risk appetite. According to Mortgage Market Survey data, 30-year fixed construction loan averages have settled near 6.2% as of Q3 2024, representing a sustained upward trajectory but one that offers both challenges and strategic windows.

Peak Rates and Their Drivers: What Pushed Construction Loans to New Heights?

The recent spike in construction financing costs stems from multiple forces converging in 2022–2023.Central bank monetary tightening—fast-tracked by the Federal Reserve to combat inflation—dramatically raised benchmark interest rates. By mid-2023, the Fed Funds Rate exceeded 5%, sending ripple effects through underwriting environments and capital availability for developers. Compounding factors include: - Balanced labor and material costs post-pandemic supply chain adjustments - Increased borrowing competition from institutional investors targeting build-to-rent portfolios - Regional demand imbalances, especially in high-growth Sun Belt and coastal markets “Construction loans are no longer just about interest spreads—they’re also a reflection of perceived project risk,” explains Mark Reynolds, Senior Analyst at Zillow Mortgage Research.

“Developers in hard-to-find land or uncertain zoning areas face significantly higher rates, sometimes exceeding 7.2%.” These elevated costs directly influence developer margins and buyer affordability, making timing and market selection strategic imperatives.

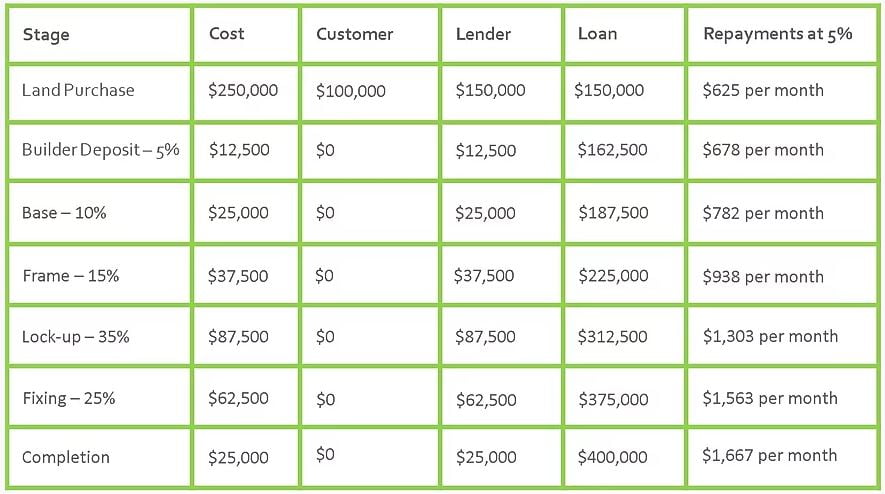

How Construction Loan Terms Shape Costs: Fixed vs. Adjustable, Rates, and Repayment Plans

Construction loans typically include two core structures: fixed-rate term loans and adjustable-rate facilities.A fixed-term loan, often 5 to 10 years with balloon or wrapper options, locks in borrowing costs for the construction period, offering stability during volatile rate cycles. In contrast, adjustable-rate construction loans introduce flexibility but carry uncertainty—especially when benchmark rates rise. Loan terms also influence effective rates: shorter terms may offer lower floating rates but demand larger upfront capital, while longer terms improve cash flow but increase total interest outlays over the build cycle.

Private lenders and hard money sources often charge premium fixed rates—sometimes 150 to 300 basis points over public market yields—due to higher risk exposure. “It’s crucial to analyze loan structure in tandem with project timelines,” notes Clara Vasquez, a lending specialist at Blue Ridge Mortgage Services. “Buyers and developers who tie rates too late may miss optimal windows.

Fixed-rate options surged in popularity in Q2 2024, as project delays stretched from 6 to 12 months.”

Breakdown of typical loan terms impacting cost: - 5-year fixed: Average 6.1% – ideal for short-cycle developments, premium pricing - 7-year adjustable: Underlying rate tied to SOFR plus margin; volatile but responsive - 10-year term with wrapper: Blends stability with rate protection at closing, widely favored in high-risk zones Lenders now stress urgent pre-qualification, emphasizing documentation precision to avoid rate fluctuations during underwriting—particularly for junior land entitlements or modular home builds.

Competitive Market Dynamics: Lender Strategies and Buyer Leverage

The construction lending arena is increasingly competitive. Traditional banks, credit unions, and specialized hard money lenders all vie for market share, often deploying targeted marketing to first-time developers and construction firms.This competition has driven greater transparency in rate quotes—many institutions now offer instant pre-approvals online, reducing friction in the borrowing process. A rising trend is pre-approval “locking,” where buyers secure rates before breaking ground, particularly valuable in tight supply markets. According to Freddie Mac data, developers securing commitments 90+ days pre-construction avoid rate hikes and secure better terms, reducing overall project financing risk by up to 20%.

Developers, especially firms managing multiple phases, leverage loan comparison tools and portfolio diversification—securing some fixed-rate commitments while leaving others adjustable—to balance cost certainty with market agility. This hybrid strategy proved effective during the 2023–2024 volatility, preserving profitability without locking in overpriced funding. “Market savvy starts with understanding lender product tiers,” says Ryan Clark, CEO of Horizon Build Capital.

“We recommend building relationships early—lancing a relationship before construction begins often yields the best pricing and terms.”

Navigating Mortgage and Insurance Fees: Hidden Costs Often Overlooked

Beyond the headline loan rate, buyers and developers must account for a range of embedded expenses that collectively define total financing cost. These include origination fees, underwriting charges, title insurance, early repayment penalties, and builder default insurance—all essential lines of protection but often underestimated. Current benchmarks show: - Origination fees average 0.5%–1.5% of loan amount - Title and settlement fees range $1,500–$3,500 for residential builds - Builder default insurance: $0.30–$0.60 per $1,000 of loan balance, mandatory in high-risk jurisdictions “Omitting these ancillary costs can inflate perceived affordability by 10–15%,” warns Sarah Lin, Chief Financial Analyst at RealPath Lending.“A $500,000 construction loan may truly carry $7,500–$10,000 in extras—hardly trivial in tight budgeting.” Lenders increasingly bundle these supplies into streamlined “destination financing” packages, though buyers must scrutinize inclusion and exclusions. Transparency in the fine print prevents unpleasant surprises down the line.

Strategic Planning: Best Practices for Locking in Favorable Rate Windows

Securing the optimal construction loan rate hinges on proactive planning and market timing.Key tactics include: - Monitor Federal Reserve announcements and inflation data weekly—rate decisions impact lender baselines every four to six weeks - Maintain a pre-construction capital buffer: 20%–30% more than project costs cushions exigencies and secures pricing ahead of market shifts - Engage multiple lenders: comparative quotes often reveal 0.3%–0.8% differences, especially for non-prime or niche borrower profiles - Fix rate windows during easing cycles: Q2 and Q4 of 2024 saw the most favorable conditions, with some lenders offering 6.0% fixed rates Developers should also consider interest rate swaps or caps as hedging instruments—particularly effective for long-duration builds susceptible to rate spikes. “The most successful projects blend financial discipline with market agility,” says Butler, co-founder of DualBuild Originations. “Rate certainty isn’t always about immediate lowest quotes—it’s about locking in terms before bottlenecks form.”

Regional Rate Variances: Why Location Drives Financing Costs

Construction loan rates differ markedly across U.S.markets, shaped by local supply constraints, tax policy, and regional risk profiles. For instance: - Coastal Midwest and Florida: Booming demand plus hurricane risk lifts rates to 6.4%–7.8% - Rocky Mountain states: Tighter land availability elevates risk premiums, averaging 6.3% - Southwest Sun Belt (AZ, TX): Competitive but variable—rates hover at 5.8%–6.8%, with Desert Sun Capital reporting sharp differentials based on tenant pre-sales Local labor costs, permitting timelines, and municipal bond incentives further refine regional pricing. Buyers eyeing multi-site portfolios should model rate exposure by metro area to optimize capital deployment.

When to Lock In: Timing Your Loan Close for Optimal Rate Capture

The moment to secure a construction loan has shifted from rigid

Related Post

Kabar Baik! Indonesia’s Latest Wave of Positivity Sparks Nationwide Momentum

Quiero Agua: The Viral Horror Video That Turned Fear into Global Obsession

Кат маленький загадка —Cat In 러시아어, mehr als nur ein Haustier

Unlock Me1 Lol Free Robux: The Complete Guide to Genuine, No-Cost in-game Currency with Me1 Platforms