2024 Car Loan Interest Rates: Your Ultimate 2024 Guide to Securing the Best Financing

2024 Car Loan Interest Rates: Your Ultimate 2024 Guide to Securing the Best Financing

Navigating the 2024 car loan landscape requires more than just understanding monthly payments—it demands awareness of rapidly shifting interest rates, lender strategies, and consumer tools that can turn a costly burden into a manageable investment. With economic forces fluctuating and consumer demand for vehicles strong, understanding current car loan interest rates is no longer optional—it’s essential for smart buyers. In 2024, the average rates reflect both recovery from inflationary pressures and regional差异, making a clear, data-driven guide more valuable than ever.

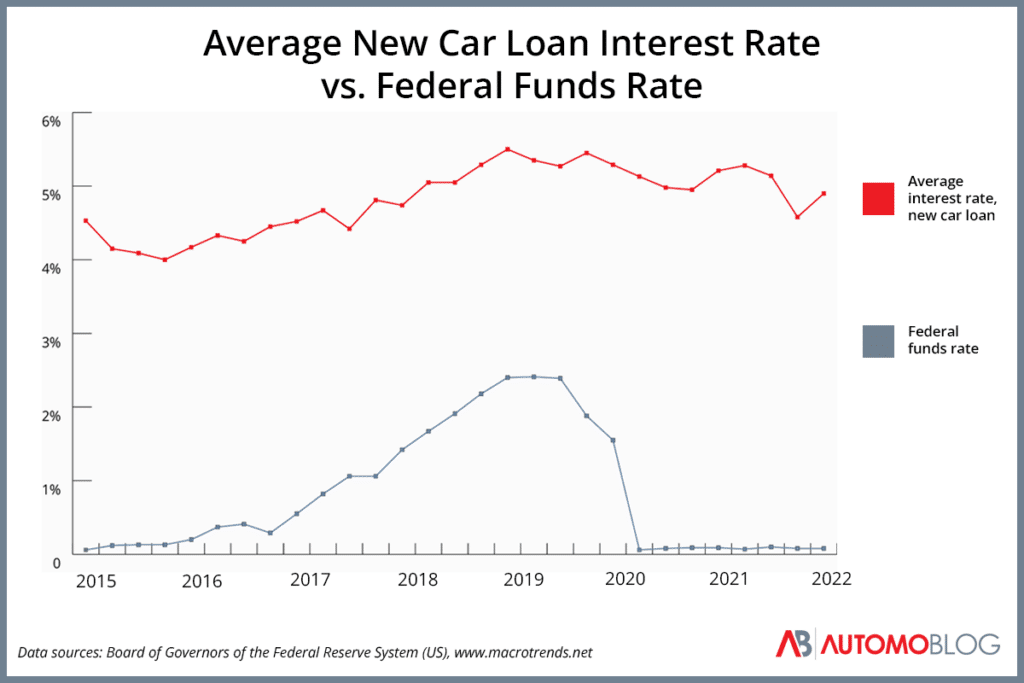

As of early 2024, national average car loan interest rates hover around 6.5% to 7.1%, marking a steady decline from the peaks of 2023 but still above pre-pandemic territory. This range represents wide variation depending on creditworthiness, loan term, vehicle type, and lender policy. For example, a borrower with excellent credit securing a six-year loan on a new electric vehicle may access rates closer to 5.8%, while someone financing a used car with an average credit score on a longer 72-month plan could face rates near 7.4%.

These figures underscore the criticality of pre-qualification and comparison shopping in reducing true borrowing costs.

Factors Driving 2024 Car Loan Rates Higher Than Recent Years

Several interconnected macroeconomic and industry factors influence borrowing costs. Central bank policy remains pivotal—while the Federal Reserve has paused rate hikes after years of tightening, the lingering posture of elevated short-term rates keeps lending costs elevated. After years of double-digit lending rates, even a fraction-point increase translates to thousands in extra interest over a standard five-year term.Supply chain recovery and inventory adjustments post-pandemic have shaped risk assessments for lenders. With vehicle supply stabilizing and existing loan defaults gently decreasing, some financial institutions are cautiously optimistic, but lingering uncertainty from geopolitical tensions and raw material costs keeps rates cautious. Furthermore, the surge in electric vehicle adoption has prompted targeted lending programs, often with slightly favorable rates for eco-conscious buyers, though these often come with promotional terms that expire quickly.

Credit Score Breakdown: How Your Rating Impacts Loan Terms

Your credit history remains the single strongest determinant of your 2024 loan interest rate.Lenders rely on FICO and VantageScore data to gauge risk: borrowers in the top quartile (750+ scores) typically access rates near 5.5% to 5.9%, enjoying terms like $30,000 financing over five years with minimal interest. By contrast, borrowers with scores in the 620–679 range often face rates above 7.0%, with some non-qualified applicants seeing rates climb past 7.5%.

Key lending thresholds to monitor: - 740+: Prime tier, near-perfect access to lowest variable rates - 670–739: Strong cottager with solid negotiating power - 580–669: Standard market, moderately higher rates - Below 580: Subprime access, with significant premium costs Lenders amplify differentiation through tiered underwriting—often offering market rates to leading credit profiles while applying steep penalties to younger or damaged credit records. This disparity underscores why credit preparation precedes loan shopping.

Loan Term Strategies: Balancing Payment Size and Total Interest

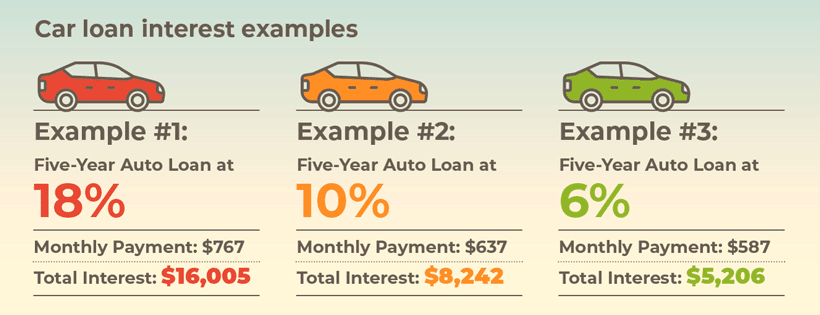

The term of a car loan—typically 36 to 84 months—dramatically shapes monthly affordability and lifetime interest. While shorter terms (36–48 months) reduce total interest by weeks of payment but increase monthly outflows, longer terms (72–84 months) soften immediate cash strain at a clear financial cost.For example, a $30,000 loan at 6.9% over five years (60 months) incurs approximately $243 in monthly payments and total paying $147,480—$17,480 in interest.

Extend that same loan to 72 months, monthly payments drop to $430 but escalate total interest to $25,440, costing $21,980 more. Selecting a term requires aligning payment capacity with long-term ownership goals. Boosting down payments further improves ripple effects—cutting principal directly lowers interest not only on loan amounts but also on future months’ charges.

Climate and Low-Emission Vehicle Hiring: Rate Incentives in 2024

Automakers and lenders have responded to sustainability goals with preferential financing for electric and hybrid models. Many manufacturers and credit unions now offer lower introductory rates—sometimes 100 to 200 basis points below standard benchmarks—for qualifying eco-friendly vehicles. These incentives can save buyers $1,000s over the loan life, though often expire after 12–24 months.Beyond incentives, program partners frequently include tax credit holder facilitation, streamlining access to federal VEII (Vehicle Electrification Incentive) disbursements. Buyers should verify eligibility, as documentation requirements—proof of purchase, certification, and credit thresholds—vary by dealership and region.

Shopping Smart: Tactics to Lock in the Best Rates in 2024

Navigating today’s crowded financing marketplace demands proactive, data-driven behavior.Multiple lenders—banks, credit unions, online originators—offer varying terms, so seeking quotes across platforms is essential. The U.S. Consumer Financial Protection Bureau advises starting the search after gross income stabilizes, ideally within 60–90 days of desired purchase.

Use online rate comparison tools to filter offers by credit tier, term, and vehicle segment. Pre-approval without hard credit checks gives visibility into expected terms. Pay attention not just to APR but also hidden fees—origination charges, prepayment penalties, and processing fees that inflate true borrowing costs.

Secret tactics: - Negotiate: Some lenders bring better offers; have alternative quotes ready. - Time matters: Rates fluctuate—seasonal trends (e.g., Q1 tax incentive rollouts) influence lender positioning. - Co-signer advantage: A trusted co-signer with strong credit can unlock 20–100 basis point drops.

For borrowers prioritizing long-term value, consider manufacturer-backed financing through dealership credit programs. Though often tied to specific models, these can offer grace periods of 90+ days—widely uncommon in traditional banking—giving time to test reliability without immediate stress.

The Path Forward: Anticipating Rate Trends in a Shifting Economy

Looking ahead, the trajectory of 2024’s elevated rates depends on broader economic stability.If inflation moderates and central banking signals rate pauses or cuts in 2025, 2026 loan pricing may stabilize—potentially approaching pre-2022 territory. Analysts project a mild normalization, driven by consumer spending resilience and mixed signals from global growth.

However, unexpected shocks—geopolitical escalations, energy market volatility, or supply disruptions—could prolong rate uncertainty.

For now, locked-in 2024 rates remain your best defense against inflation-driven erosion, especially for buyers locking funds months before delivery. The 2024 car loan environment is marked by cautious optimism, careful risk management, and strategic planning. By understanding rate drivers, optimizing credit profiles, choosing smart terms, and leveraging regional incentives, consumers can secure financing that protects both wallet and long-term financial health.

This is not just about buying a car—it’s about building smarter ownership through informed, timely decisions.

Related Post

/cdn.vox-cdn.com/uploads/chorus_image/image/65143535/1025667282.jpg.0.jpg)

Wyoming vs. Colorado Buffaloes: A Statistical Farmhouse Showdown That Redefines Inter-Mountain Rivalry

Ismaili TV: Bridging Faith, Culture, and Global Storytelling in One Streaming Space

IPad 3: The Power Upgrade You Didn’t Know You Needed – Performance, Updates, and Reality Check

What Is Atlanta Time Now? Understanding the Heart of Georgia’s Time Zone